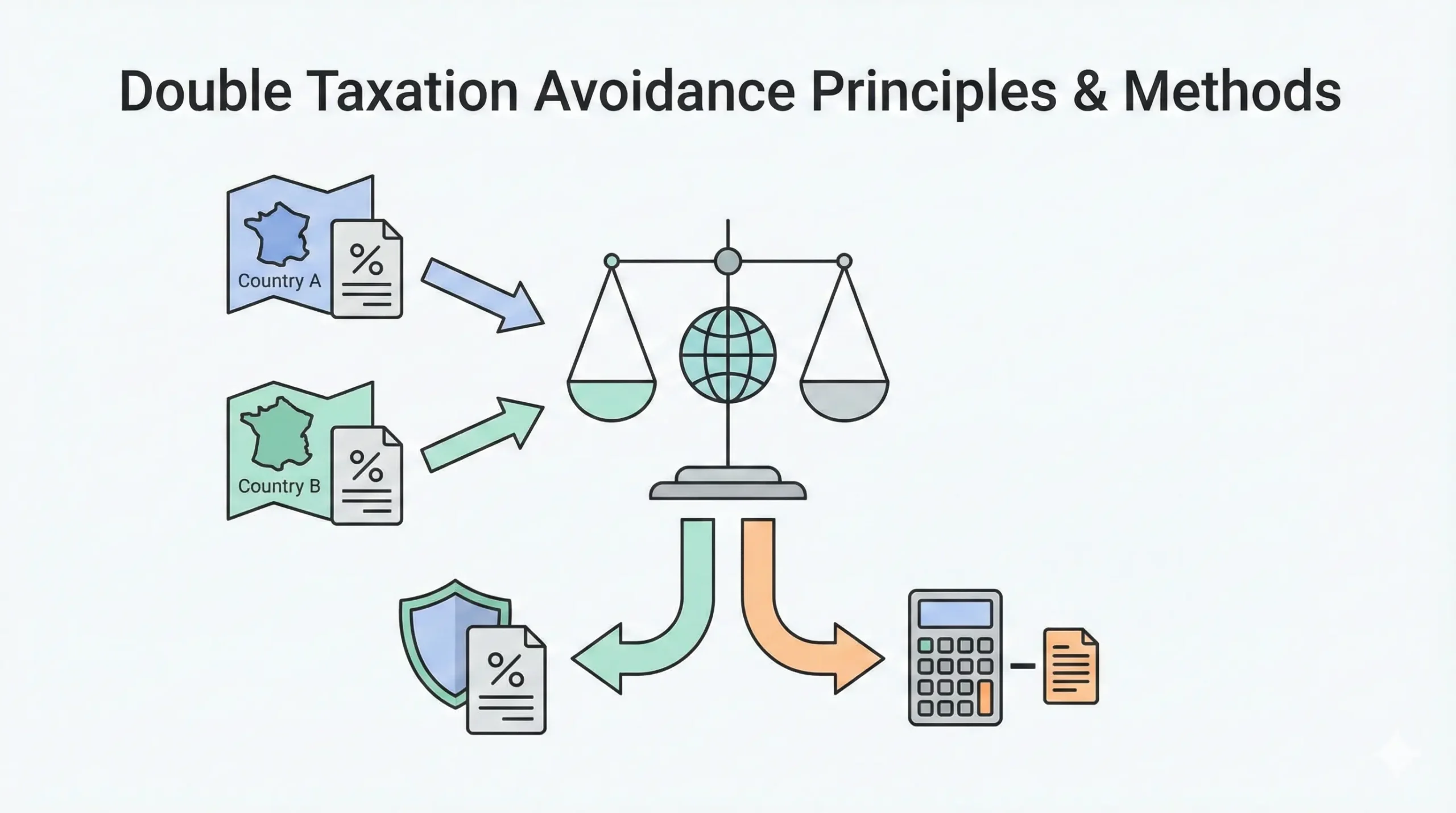

The major financial obstacle to international trade and cross-border investments is the risk of the same income being taxed in both the country where the income is generated (Source Country) and the country where the earner is resident (Resident Country). Double Taxation Avoidance Agreements (DTAA) are treaties based on international law, signed between two countries to eliminate or reduce this duplicate tax burden. In Turkey, pursuant to Article 90 of the Constitution, duly enacted DTAA provisions take precedence over domestic laws (such as Corporate Tax and Income Tax Laws).

The foundation of the application rests on correctly determining the taxpayer’s status.

Fiscal Domicile (Residency): The status that determines in which country a person or entity is subject to full tax liability on their worldwide income. Only “Residents” can benefit from a DTAA.

Permanent Establishment (PE): The situation where an enterprise has a fixed place of business (branch, office, factory, construction site, etc.) through which it carries on all or part of its commercial activities. The right to tax business profits is generally granted to the country where the PE is located.

2. Methods of Relief: Exemption vs. Credit

Treaties primarily use two main methods to avoid double taxation. Which method applies is determined by the specific article of the relevant treaty.

Analytical Comparison Table

Feature

Method A: Exemption Method

Method B: Credit Method

Basic Principle

Income taxed in the source country is completely exempt from tax in the resident country.

Tax paid in the source country is deducted (credited) against the tax calculated in the resident country.

Application in Turkey

Less common. Usually applied as “Exemption with Progression.”

The primary method in most treaties signed by Turkey (Based on KVK Art. 32).

Taxpayer Advantage

More advantageous if the tax rate in the source country is lower than in Turkey.

The total tax burden usually equals the higher tax rate between the two countries.

Bureaucratic Burden

Low / Medium

High (Requires proof of foreign tax payment).

📌 Practice & Additional Info: The existence of a DTAA does not automatically mean “zero tax” will be paid. Treaties usually allocate the taxing right between the two countries or place an upper limit (e.g., 10% withholding tax) on the tax rate in the source country.

Frequently Asked Questions

Does having a treaty automatically reduce tax?

No. Treaty provisions do not apply automatically. The taxpayer must declare their intent to benefit from the treaty to the relevant tax office and submit the necessary documents (such as a Certificate of Residence).

What are Tie-Breaker Rules?

These are hierarchical rules used to determine which state will be considered the sole state of residence for treaty purposes when a person or entity is considered a “Resident” under the domestic laws of both states (dual residency) (e.g., permanent home, center of vital interests).

Does Turkey have agreements with all countries?

No. As of 2025, Turkey has agreements in force with over 80 countries, but not with every country in the world. For countries without an agreement, domestic law rules (unilateral credit) apply.

Professional Support

DTAA applications are a complex area where international tax law intersects with local legislation. Choosing the wrong method or missing documentation can lead to duplicate tax payments or penalties. You can rely on Vergi Merkezi expertise for international tax planning and treaty applications.

For Online Services and Information Contact Us

Ready to establish or grow your business in Turkey? Contact Vergi Merkezi | Mali Müşavirlik today for a consultation with our expert accountants.

")

")

Bir yanıt yazın